Non-standard insurance is no longer exceptional. The nature of risk is ever evolving as the way we live continues to change. Factors such as climate change are becoming a much bigger issue and have significant implications both for insurance providers and homeowners.

The evidence of this shift is all around us. Just this week, Lloyd’s of London announced that they have seen steep losses over the last two years due to natural catastrophes. This announcement followed the news that hundreds of Whaley Bridge residents were forced to evacuate their homes after extreme rainfall threatened to burst a nearby dam. Even MPs have come forward recently suggesting that companies are going to have to be more forthcoming about the risk their assets face as a result of climate change. The insurance market is going to have to adapt.

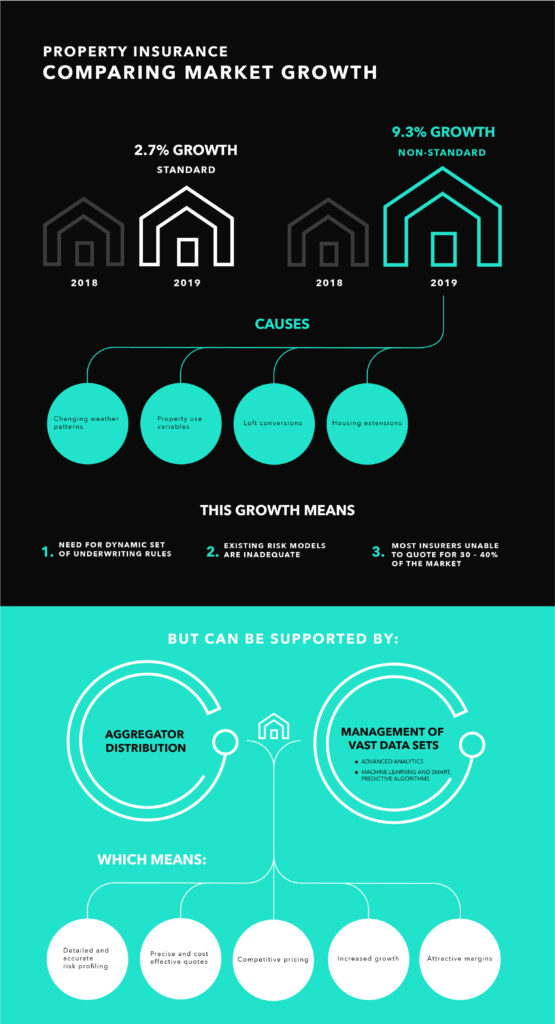

Climate issues aren’t new, the UK heatwave of 2018 led to increased subsidence, while the growth of flood plains has had a similar effect with more and more homes being pulled into the non-standard category. In fact, just looking at the shoparound market, the non-standard category saw year-on-year growth of 9.3 per cent from 2018 to 2019, compared to the 2.7 per cent growth seen in the standard market.

But it’s not all down to climate change, the rise of non-standard is also largely due to the changing nature of housing stock. A 19th century family villa comes with very different risks to a new-build flat. Seemingly innocuous factors such as whether the house has multiple occupants, serves as a work-living space, houses a lodger, or Airbnb guests, changes the profile once again.

Additionally, the nation’s embrace of loft conversions and extensions – invariably flat-roofed – is altering the national risk profile at scale. The current economics of home-buying suggest that renovating will remain at least as popular as buying, and that the rate of second (and thus frequently empty) home ownership will grow.

Unfortunately, many homeowners only discover their non-standard status when they apply for home insurance. These consumers naturally expect exactly the same services as their standard counterparts. They don’t want to be treated differently, they expect instant quotes, competitive prices, online transactions, and easy self-serve options, and insurers who can’t deliver this risk losing customers.

Because, of course, even as the category grows non-standard is still just that. It seems that insurance providers have found it too hard to meet the needs of this new category without risking their loss ratios. Consequently, most insurers only have an underwriting footprint of 60-70 per cent. Now that non-standard is rapidly becoming the new normal, this is no longer sustainable.

However, the good news is that the rise in non-standard can be supported by two major technology trends. The first, aggregator distribution, democratises the process of getting a quote and gives consumers a more complete view of their options, leading to an increased underwriting appetite for non-standard markets. This results in a virtuous circle, in which the number of brands prepared to quote online for non-standard is growing, increasing the viability of aggregators as a distribution route for non-standard products, which has increased customer engagement in turn.

The second trend is set to have an even bigger impact: the technical ability to manage, process, and analyse previously unthinkable volumes and varieties of data. Advanced analytics, machine-learning techniques and smart predictive algorithms give a much more detailed and accurate risk profile – leading to more precise and cost-effective quotes which is positive for both insurers and the consumer.

Climate change may be accelerating changes in the insurance market, but there are many reasons why non-standard is on the rise, bringing different risk dynamics with it. Standard price and risk modeling are struggling to respond, and a more dynamic set of underwriting rules is required. While not every underwriter will have the technological tools to cope, and not every organisation will choose to be competitive in this market, for those that do, they will face both attractive margins and a growing consumer audience.